Try to talk about “natural capital” or “ecosystems services” to business leaders. Their eyes get glazed. Not only are these terms too academic and scientific for the business community, there is great discomfort in discussing anything the company has no perceived control over. To dig deeper into how companies are learning the language of sustainability and applying it to their business, I spoke with six organizations that advise businesses on sustainability and external impact assessment. Several themes emerged from these discussions that gave rise to best practices in communicating sustainability, increasing sustainability-literacy and propelling organizations toward complete integration of sustainability metrics in corporate management systems.

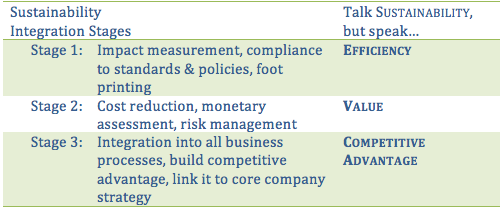

Sustainability integration can be broken down into three stages ranging from physical impact measurement to the integration of sustainability into the core management systems that drive business strategy. While “talking sustainability” at each stage, it is important to “speak business” to convey relevance and inspire the organization to reach for the next stage of sustainability integration.

Stage 1: talk Sustainability, but speak Efficiency

Stage 1 is the gateway to true sustainable transformations. Characterized by physical impact measurement, such as carbon emissions, water footprint and material consumption, sustainability’s proverbial foot in the door is “efficiency.” In business language this means resources, raw materials, time, space; man-hours per widget, rolls per square feet of factory, utilization rate…. These are the things that business can control directly and about which operations managers feel comfortable engaging in discussion. Language representative of Stage 1 sustainability integration includes:

- Increased efficiency

- Reduced turnover

- Reduced intensity

- Increased throughput

- Footprint

Stage 2: talk Sustainability, but speak Value

Stage 2 begins to connect the measured impacts of Stage 1 to monetary value. All the efficiencies, reductions and increased throughput can directly and confidently be translated to money saved and earned by internal accountants. Inspired by the first stages of sustainability success, organizations become more willing to explore other areas of the value chain out of their direct control on which they could have significant impact. This is the stage at which the language of “materiality” can be introduced as organizations begin to realize that programs to improve sustainability metrics are significant to the bottom line and are important in the eyes of the SEC (in the US) and important stakeholder groups. The physical impact assessments of Stage 1 also leads to risk assessment and valuation of loss should they no longer have access to a raw material or lose the right to operate in a stressed region. Smart organizations develop sustainability strategies to take advantage of cost savings and reduce future risk. Talking Sustainability, but speaking Value uses such language as:

- Cost reduction

- Risk management

- Value chain

- Supply management

- Engagement

- Materiality

Stage 3: talk Sustainability, but speak Competitive Advantage

Organizations move from Stage 2 to Stage 3 when they realize that sustainability offers a competitive advantage. The sustainability metrics and value capture implemented in Stages 1 and 2 become embedded into the corporate management systems rather than as separate, “tacked-on” exercises. The reactive nature of Stage 1 and 2 strategies to improve efficiency and reduce risk transform into proactive strategies for process and product redesign that capitalizes on consumer demand and decouples the growth of the company from increasing resource scarcity. These strategies become central to the overall business strategy and are directly linked to the business mission and purpose. The lines defining sustainability and business-as-usual bleed together as organizations move toward integrated reporting. The value of ecosystem services finally becomes an approachable topic for enhancing corporate strategy. The use of conventional sustainability terms increases at organizations in Stage 3 with such phrases as:

- Societal Value

- EP&L (Environmental Profit & Loss)

- Natural capital and ecosystem services

- Regeneration

- Life cycle assessment

- Circular economy

By addressing each organization in the language appropriate to their respective stage, businesses can be made more comfortable with the changes they need to make to become more sustainable. It is important to recognize that metrics and values used throughout the process, which is seldom linear, are only representations of what matters; the process of sustainability integration is a tool that is best used in the spirit of making a more sustainable world. In the words of Albert Einstein, “Not everything that can be counted counts, and not everything that counts can be counted.”

BIO

Katie is a Strategy Analyst with over 10 years of experience advising B2B and B2C clients on capital investment strategies through linking market trends to company assets and capabilities across forest products, pulp and paper, and consumer goods. Currently based in Beacon, NY, she is passionate about improving the sustainability of the things we use every day by integrating of sustainability into corporate decision-making processes.

www.linkedin.com/in/KatieMencke

www.facebook.com/bardmbainsustainability