Hyman Minsky is probably best known for his work on financial instability and financial reform, but he also wrote extensively about how to address the persistent problem of all those left behind by our increasingly financialized economy; about how to design policies that would put an end to income poverty in the midst of plenty. Despite the fact that far more attention has been paid to his writing on financial fragility, these were intimately related issues in Minsky’s research, connecting the financial and “real” economies.

As with his work on finance, Minsky’s approach to poverty did not fit comfortably within the confines of the status quo. With “trickle-down” on one side, pure tax-and-transfer approaches on the other, and vague calls for retraining floating somewhere in the middle, Minsky found the conventional menu of policy options incomplete and inadequate (a menu that has changed very little over the last several decades). Calling for “upgrading” workers without ensuring there are enough jobs to go around is, as Minsky put it, “analogous to the great error-producing sin of infielders — throwing the ball before you have it.” What’s missing, he thought, is a commitment to ensuring that paying jobs are available to all who are ready and able to work; a commitment to “tight full employment.” The question is how to get there without sparking runaway inflation or inducing financial crises. Private markets, left to their own devices, aren’t going to get us there. For part of the answer, Minsky turned to a forgotten side of the New Deal: direct job creation.

In the interests of providing a more complete picture of Minsky’s intellectual legacy, the Levy Institute has published a collection of his central writings on poverty and full employment: Ending Poverty: Jobs, Not Welfare. The chapters span roughly three decades of Minsky’s writing and feature four never-before-published pieces. The earliest were written in the context of the “War on Poverty” of the Kennedy and Johnson years, but readers will find more than mere historical interest here. Minsky’s critiques of both the “neoclassical synthesis” and the welfare state hold up rather well. If anything, the material is even more relevant today, given our widening income inequality and chronic rates of long-term unemployment — and the fact that the battle against poverty, while not won, has largely been forgotten.

The paperback is now available on Amazon; the Kindle version will be appearing shortly.

Here are today’s big pieces of economic policy news: (1) net job creation in the month of March (+88,000) was too low to keep up with population growth; (2) the president’s budget proposal will reportedly include cuts to Medicare and Social Security (or as the latter will be described in most newspapers, “adjustments to the way inflation is calculated for the purposes of determining Social Security benefits”).

These two items may seem unrelated, but in reality they form the basis of an unhappy remarriage. continue reading…

There have been many concerns expressed on the internet about the eventual necessity of reversing the Fed’s cheap-money policies, which include “quantitative easing,” as well as a near-zero federal funds rate.

One idea some have is that there are “too many bonds” in the Fed’s portfolio, and that problems will occur with insufficient demand whenever the Fed attempts to reduce its holdings. This doomsday scenario often seems to vex public discussion but is unlikely to materialize, given that the Fed can always make use of its ability to “make a market” for Treasury securities.

An alternative way of looking at the same situation is that there is a huge amount of money and money-equivalents on bank balance sheets and in nonfinancial corporate coffers, and that the tendency of the modern economy toward financial fragility will eventually lead to risky loans and investments using these funds. (Jeremy Siegel adopts this view in the FT, with, however, an unfortunate emphasis on the possibility of a takeoff of inflation. Inflation remains below the Fed’s 2-percent approximate objective, and the greater risk by far is still recession. An Alphaville comment on his column makes the point that the threat of fragility remains regardless of whether banks have excess reserves on hand.) Concerns have already emerged about “junk” bonds, so-called leveraged loans, and other effervescent areas of finance. Of course, the problem then becomes for the authorities to implement an appropriate restraint on financial excesses. One conventional method would be to increase interest rates using open-market operations, which would of course probably entail the sale of securities. This scenario unfortunately might lead to some serious threats to financial stability, including problems that short-term and/or variable-rate borrowers might have meeting payment commitments on their debts, if the Fed were to raise interest rates sharply.

One big historical example of this kind of fragility is the rise in short-term interest rates that occurred in the late 1970s and early 1980s at the behest of the Fed. The resulting delta-R effect helped to bankrupt Mexico, among other disastrous impacts. Many years before that, the Fed was more inclined to use direct controls on credit, restricting the amount of money banks could lend out.

Key to the situation today, efforts are ongoing in Washington to formulate and implement appropriate rules to insure that various kinds of bank lending do not get out of hand in the first place. Efforts of this type would be unlikely to completely prevent future crises, but, if effective, would act to reduce fragility. Among other benefits, this approach might also permit the recovery in housing investment—currently only in a fledgling phase—to continue. Given the problems that sharp interest-rate increases can bring, it would also be helpful to keep the effects of moderate inflation in perspective, and to cope with inflation in non-destabilizing ways.

An update on some developments on the fiscal-trap front: After a Levy brief on fiscal traps was issued in November, events continue to bear out the fears expressed therein that budget cuts and tax increases being implemented in Europe and the US would lead to disaster. For example, recent news coverage of events surrounding the announcement of the UK budget confirm that the trap can hit nations that possess their own currencies, particularly in a region such as Europe where recessionary forces are dominating at the moment. Martin Wolf notes that owing to disappointing growth figures, the UK deficit surprised again on the high side. As the fiscal-trap theory asserts, governments implementing austerity policies have run into unexpectedly low growth in their attempts to reduce government debt.

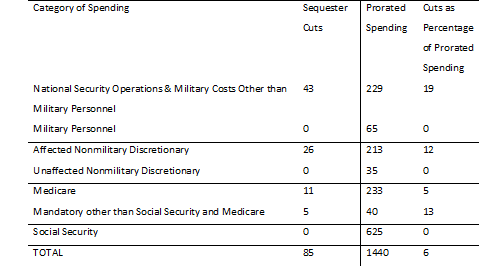

Meanwhile, despite the warnings of macroeconomists, including those here, the austerity measures that together make up the fiscal cliff in the US were only partly averted. Among these policy changes are the loss of the 2-percent partial payroll-tax holiday and the sequester cuts to discretionary spending. The latter unfortunately went into effect at the beginning of this month, following a two-month Congressional reprieve. Based on unofficial data from the Bipartisan Policy Council in this New York Times article, which are similar to those in a recent and more detailed CBPP report, the cuts for the remainder of the fiscal year are large as a percentage of planned spending, as seen in Table 1:

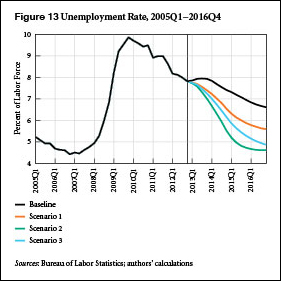

How much fiscal stimulus would the government need to inject into the economy over the next two years in order to get the unemployment rate into the 5.5–5.9 percent range? In their newest strategic analysis, Dimitri Papadimitriou, Greg Hannsgen, and Michalis Nikiforos provide us with some harrowing answers.

The authors lay out a scenario (“scenario 3” in the analysis) featuring some favorable macroeconomic tailwinds in the form of higher private sector borrowing and increased exports. As they explain, such developments are not entirely unlikely (and policy changes could help contribute to such an export boost). Nevertheless, even in these relatively rosy circumstances the government would need to pitch in a spending increase of 6.8 percent* (after inflation) in each of 2013 and 2014 to bring the unemployment rate below 6 percent by the end of 2014. That would amount to a stimulus program worth around $600 billion over the next two years. Without these tailwinds from private sector borrowing and exports (“scenario 2”), spending would need to increase by 11 percent per year — or roughly over a trillion dollars of stimulus over two years — in order to bring unemployment down to around 5.5 percent.

As the authors note, Washington is not in the mood for a trillion-plus-dollar stimulus program, or a program half that size. Congress has consistently rejected a mere $50 billion for infrastructure repair. If anything, the policy challenge of the moment is to temper the zeal for cutting spending. Moreover, 5.5 percent unemployment is arguably still shy of what we ought to consider “good enough.” This level is around a full percentage point above where we were before the recession hit in 2007. In other words, even if this Congress were to approve a stimulus package larger than the 2009 Recovery Act (ARRA) — which is unimaginable at this point — we would still not be back to pre-recession unemployment levels after two years (or even four years, as the strategic analysis demonstrates).

While we’ve been focused on phantom budget menaces derived from assumptions about the state of medical technology in 2080, the jobs crisis has continued to ruin real lives. Without a dramatic turnaround in our fiscal priorities, it will continue to do so for years to come. It’s become pretty clear that the actual needs of this economy far outstrip what the political system is willing to deliver. (The authors actually favor direct job creation, in the form of an employer-of-last-resort policy, but they suggest that this is currently even further outside the realm of the politically possible as compared to traditional fiscal stimulus.)

Assuming no further stimulus is possible, the “best case” scenario over the next four years might be to merely hold off any new attempts at grand bargains or further budget cuts; to maintain the miserable status quo on the budget. In that case, as the figure below illustrates (the authors’ “Baseline” forecast represented by the black line), unemployment would still be above 7 percent in two years, and above 6.5 percent by the end of President Obama’s term in office (which, as the authors point out, is still in excess of the threshold at which the Fed would consider tightening monetary policy).

Earlier this month the Athens Development and Governance Institute and the Levy Economics Institute held a forum on the eurozone crisis: “Exiting the Crisis: The Challenge of an Alternative Policy Roadmap.” Below are the remarks delivered by senior scholars Jan Kregel and James Galbraith.

In a new, wide-ranging policy note, C. J. Polychroniou traces the roots and evolution of the present “era of global neoliberalism”; an era he portrays as mired in perpetual crisis and dysfunction, and ripe for change.

[N]eoliberalism itself is more of an ideological construct than a solidly grounded theoretical approach or an empirically-derived methodology. In fact, the intellectual foundations of neoliberal discourse are couched in profusely vague claims and ahistorical terms. Notions such as “free markets,” “economic efficiency,” and “perfect competition” are so devoid of any empirical reference that they belong to a discourse on metaphysics, not economics.

Polychroniou attempts to outline the central principles of a progressive, post-Keynesian economic policy alternative. His primary target: changing the relationship between the state and the financial sector.

Yesterday, Dimitri Papadimitriou joined Ian Masters to discuss the response to the banking crisis in Cyprus. The plan on the table, in which Cypriot banks would impose a deposit tax (9.9 percent on deposits above €100,000, and 6.75 on deposits below that) in order to gain access to a €10 billion bailout from the troika, unconscionably makes small depositors pay for someone else’s regulatory blunders — and is likely to be ineffective anyway, said Papadimitriou.

The entire episode once again points to the fundamentally unworkable setup of the eurozone, in which each member-nation is (ostensibly) responsible for its own banking system. For more on these deeper structural problems, see this policy note: “Euroland’s Original Sin.”

Victoria Chick, a student of Hyman Minsky’s, elaborates on an issue that often strikes non-economists as somewhere between scandalous and baffling: the absence of any substantive acknowledgment of money in much of contemporary economics and economic modelling.

(Particularly interesting around the 12:10 mark, where Chick argues that faulty or outdated language in relation to banking helps reinforce misunderstandings about deposits, lending, and the relationship between the two.)

ShareThis

ShareThis