Narayana Kocherlakota is the head of the Federal Reserve Bank of Minneapolis and is known for an uncommon feat in high-level policy circles: he changed his mind. Originally a monetary policy hawk, Kocherlakota has become a supporter of looser Fed policy. He spoke recently at the Levy Institute’s Minsky conference in New York, and some reports of the speech–at least as rendered by headline writers–may create the impression that Kocherlakota has been reconsidering his conversion.

“Kocherlakota Says Low Fed Rates Create Financial Instability,” one publication announced. In fact, what Kocherlakota said (see the full speech below) was far more nuanced (and to be fair, most of the media reports grasped the key points. I’m told it’s fairly common for reporters not to write their own headlines). He argued that low-rate policy can create phenomena that are commonly taken to be signs of financial instability: “unusually low real interest rates should be expected to be linked with inflated asset prices, high asset return volatility and heightened merger activity. All of these financial market outcomes are often interpreted as signifying financial market instability.”

If low interest rates created financial crises of the sort that tanked the global economy in 2007/2008, this would be a pretty good argument for siding with the hawks. But Kocherlakota’s actual, stated views are perfectly consistent with a zero-interest-rate policy creating only signs of instability. The cost-benefit analysis facing the central banker therefore looks more like this, according to Kocherlakota (his emphasis): “On the one hand, raising the real interest rate will definitely lead to lower employment and prices. On the other hand, raising the real interest rate may reduce the risk of a financial crisis—a crisis which could give rise to a much larger fall in employment and prices. Thus, the Committee has to weigh the certainty of a costly deviation from its dual mandate objectives against the benefit of reducing the probability of an even larger deviation from those objectives.”

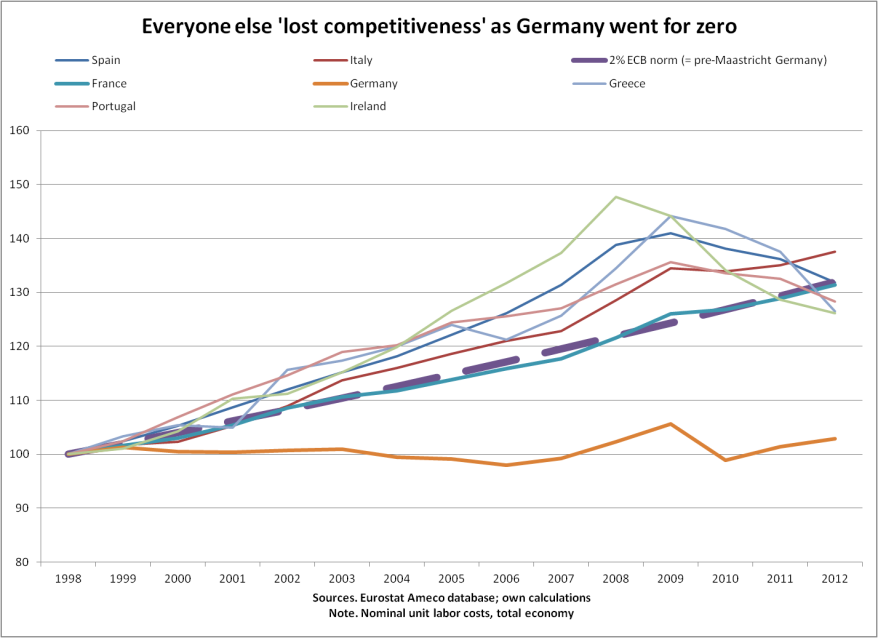

In economics, there is a remarkable “stickiness” in bad ideas and confusions. In fact, some bad ideas and confusions never seem to go away. For instance, last summer Martin Feldstein bravely suggested that euro weakening would help solve the euro crisis and rescue Europe (WSJ: “A weaker euro could rescue Europe”). Similarly, in a Bruegel Institute Policy Brief also published last summer and titled “Intra-euro rebalancing is inevitable but insufficient,” Zsolt Darvas argued that euro weakening was badly needed to restore competitiveness of euro crisis countries whose perceived inability to rebalance their external positions was a major root of the euro crisis. More recently, these two issues, euro external competitiveness and intra-euro competitiveness imbalances, were also bundled together in a piece by David Keohane titled “Why strength could be the single currency’s undoing” (FT.com 17 April 2013). Mr. Keohane seemed to identify a “euro paradox,” or even two paradoxes actually. One apparent paradox is that policy measures by the euro authorities that boost confidence in the euro run the risk of doing damage to it by undermining its long-term existence through enticing euro strength, which would postpone an export-led recovery. The other seeming paradox is that the single currency cannot exist at different levels for different countries and that it will therefore always be expensive for some and cheap for others.

Unfortunately, euro weakness as the supposed solution to the euro crisis is a thoroughly misguided piece of advice. The idea about the euro being expensive for some but cheap for others at its current level is nothing else but the external mirror image to the fact that competitiveness positions inside Europe’s currency union are utterly unbalanced – which led to corresponding intra-area current account imbalances and debt overhangs. While this is a correct diagnosis of intra-euro imbalances, implying a need for rebalancing, it must be stressed that there was absolutely nothing inevitable about this outcome. It was just that, contrary to the requirements of a currency union, Euroland simply failed to keep unit-labor cost trends within the union aligned with the commonly agreed two-percent inflation norm. In particular, as Germany stabilized its nominal unit labor cost trend at zero under the euro, the country turned űber-competitive in due course as a result. This resulted in the buildup of excessive current account surpluses – with corresponding German exposure to debts issued by its euro partner countries and exuberantly gobbled up by German banks and investors.

Perversely rewarded by the markets, Germany is imposing competitive austerity on its uncompetitive partners as the cure-all that is supposed to restore stability as well as growth. Quite predictably, the result of allegedly “growth-friendly” continent-wide austerity is catastrophic. Domestic demand in the eurozone has been shrinking for over a year now, at an annual rate of around 2 percent. The decline in GDP has been contained to less than one percent only due to a very sizable positive growth contribution from net exports. continue reading…

In recent days both Brad DeLong and Paul Krugman have written good pieces arguing against the austerity marketed by deficit hyperventilators. We can thank Thomas Herndon’s muckraking that pushed the topic front and center, showing that there is no empirical evidence in support of the austerian’s claim that big government debts slow growth.

Here’s Krugman’s argument. To briefly summarize, historical experience has demonstrated that the “growth through austerity” argument is false. Further, the monetarists have also got it wrong: monetary policy won’t get us out of this recession trap; what we really need is a good dose of fiscal policy. Given that we are in a “liquidity trap,” we can safely expand government spending without worrying about the usual downside to deficits. And in a liquidity trap, there is really no difference between Modern Money Theory and the conventional ISLM analysis. It is only once we return to a more “normal” situation that budget deficits would “matter” in the sense that they’d cause problems.

DeLong amplifies the argument here. Once we’re out of the liquidity trap, then sustained budget deficits will push up interest rates and crowd out private spending (especially investment). This is basic ISLM stuff. For those who have not taken intermediate macro, it is enough to know that in current conditions increasing budget deficits will not raise interest rates because the private sector welcomes all the liquid and safe government debt it can get. Further, flooding the economy through Quantitative Easing will not cause inflation because, again, everyone wants liquidity and would rather hold it than spend it. In more normal times, budget deficits and money helicopters would cause inflation and rising interest rates. And that would be bad.

Note, both of them raise additional good arguments against the R&R results and against austerity more generally. I am focusing in on the one point about the liquidity trap for the purposes of this blog simply because it seems to be the sticking point that prevents them from fully embracing MMT. From the perspective of Krugman and DeLong, MMT is fine for the liquidity trap, but wrong for the normal situation—when deficits will matter.continue reading…

When top managers at our largest financial firms claim to have been oblivious of dangerous financial practices carried out under their watch, the most serious implications for regulatory reform don’t actually follow from scenarios in which these managers are lying. It’s a bigger deal, in terms of how far we need to go in changing the way we regulate the banking system, if they’re telling the truth.

Bad apples, after all, can be replaced. But what if the ignorance is real; if managers really don’t know what’s going on in the units below them due to the sheer complexity of the financial institutions they’re running? This might be thought of as a convenient excuse; a universal “get out of jail free” card. But if true, it has more far-reaching, radical implications than most Bankers Behaving Badly scenarios, because it points to a problem that touches on the very structure of the financial system and its key institutions.

This, says Jan Kregel, is part of the the deeper lesson of JP Morgan Chase’s “London whale” fiasco. In a new policy brief, Kregel reviews the recent Senate Permanent Subcommittee on Investigations report on JP Morgan Chase’s difficulties and draws out the lessons for financial reform:

The most probable explanation of the misinformation concerning the “London whale” affair is a massive failure of managerial direction and control that was not the result of deliberate deception, but rather the natural response of individuals who were being paid handsomely to take responsibility but simply did not know what was going on because the size and complexity of the organization made that impossible—again, evidence of an institution that was too big to manage effectively and, a fortiori, too big to regulate.

And as Kregel emphasizes, although it’s not size per se that is problem, but rather the complexity of the institution, there’s often an intimate connection between them: “While complexity is clearly a bigger threat to financial stability than large size, it is usually, but not only, large size that induces complexity.”continue reading…

France and Germany held largely contradicting hopes and aspirations for Europe’s common currency. To France the key issue in establishing a European monetary union was to end monetary dependence, both from the vagaries of the U.S. dollar and from regional deutschmark hegemony, and to establish a global reserve currency that could actually stand up to the dollar as part of a new international monetary order. By contrast, the main German concern was to forestall the threat of deutschmark strength as undermining German competitiveness within Europe. Reserve currency status and currency overvaluation stand in conflict with Germany’s export-led growth model.

In light of the euro crisis both nations are bound to reassess the euro’s viability. No doubt France has seen all its hopes for the euro disappointed. France is facing the prospect of a lost generation today, a prospect shared with other debtor nations in the union, and a prospect that undermines the Franco-German axis and may soon turn it into the ultimate euro battleground.

Today’s GDP report estimated that the US economy grew at an annual rate of 2.5 percent in the first quarter of 2013. If the economy were translating GDP growth into jobs at rates similar to those seen in the past, this 2.5 percent pace would not get us to full employment until, say, the end of Hillary Clinton or Jeb Bush’s second term. But evidence suggests that, in fact, the link between output and jobs has been weakening for the past thirty years or so. In other words, we need higher growth rates today than we did thirty years ago to produce the same employment increases. In that context, 2.5 percent growth is nowhere near good enough.

In a new policy note, Michalis Nikiforos looks closely at US employment recovery (or lack thereof) after the “Great Recession.” In part, the dismal job creation record — which, says Nikiforos, is more accurately reflected by looking at the total number of employed workers rather than just the unemployment rate — is due to slow growth rates. Such slow growth is to be expected for an economy recovering from a financial crisis, he explains: “following the burst of a bubble and a financial crisis, the private sector seeks to minimize the debt it accumulated before the crisis. This leads to a large private sector financial surplus, which in turn weakens demand and thus output growth.”

But in addition to these slow growth rates, Nikiforos details the increasingly weak link between output growth and job creation: “[D]uring the recovery in the second half of the 1970s,a 1 percent increase in output led to an increase in employment of 0.714 percent. This number has been decreasing since the late 1970s and stands at 0.288 in the current recovery (i.e. 2009Q2–2012Q4).” In the policy note he runs through some possible reasons for this degraded link between output and jobs (including some research from a forthcoming paper by Deepankar Basu and Duncan Foley that points the finger at the growing share of the financial sector in GDP, which, they argue, leads to an overestimation of real economic activity). To give a sense of the challenge we’re facing, Nikiforos observes that just bringing the unemployment rate down to 5.5 percent by the end of 2014 would require the economy to grow at an annualized rate of 3.4 percent this year and 6.3 percent next year.

The 22nd Hyman P. Minsky conference, “Building a Financial Structure for a More Stable and Equitable Economy,” is underway. Today featured speeches by James Bullard of the St. Louis Fed, Eric Rosengren of the Boston Fed, and Thomas Hoenig of the FDIC.

This year’s event combines the Minsky conference’s usual focus on financial stability and financial reform with another of Minsky’s abiding intellectual interests: full employment policy. This was reflected in today’s varied panel sessions on measuring inequality, Minskyan employment policies, and the current state of financial regulation.

Follow the second and third days of the conference, livestreamed here. Tomorrow will feature Narayana Kocherlakota, Sarah Bloom Raskin, Alan Blinder, James Galbraith, Jan Kregel, and L. Randall Wray, among many others.

Audio of all sessions and speakers is posted here; media coverage can be found here in the press room.

Jan Kregel speaks at INET’s “Changing of the Guard?” conference in Hong Kong about the tensions between China’s highly regulated financial system and its efforts at rebalancing. Kregel compares elements of China’s financial system to what the United States had under Glass-Steagall and observes that, similar to the US experience, a de facto liberalization is occurring in China through the emergence of shadow banking:

The President’s budget has arrived and, as reported, it does contain proposed cuts to Social Security (through adopting a different measure of inflation called “chained CPI”). The emerging consensus seems to be that this is mainly intended as a political/messaging ploy. The idea here is that Republicans are extremely unlikely to make a deal that contains any revenue increases on high-income-earners; even one that includes the entitlement cuts they have (sort of) demanded. As a result of the President putting these cuts on the table in so public a fashion, so the theory goes, centrist op-ed writers will finally drop the false equivalence and declare that Republicans are being intransigent and are not negotiating in good faith toward a grand deficit-reduction bargain.

Paul Krugman points out that this is an exceedingly unlikely scenario. But even if DC pundits play along, here’s a question about this gambit that I don’t think has an obvious answer: what’s supposed to happen next? What’s meant to be the tangible payoff of the new narrative that would be created by all these editorial spankings?

Put it this way. What will have a bigger impact on a (generally more elderly) midterm electorate in 2014: ads about Republican obstinacy featuring sorrowful quotations from Fred Hiatt, or ads savaging Democrats for trying to slash Social Security? Charges of hypocrisy are unlikely to carry much weight with an electorate that suffers no cognitive discomfort in demanding that “spending” be cut but “Social Security” preserved or strengthened, and they’re even less likely to work if a voter is unaware that Republicans have even mentioned chained CPI as part of their wish list. In fact, it’s hard to see how the overall message wouldn’t just boil down to this: Republicans are being stubborn … in refusing to go along with very unpopular cuts. How many more House and Senate seats will that deliver to the President’s party?

In the LA Times, Dimitri Papadimitriou explains that the link between growth and employment has been steadily weakening over the last several decades, and that this makes getting help from fiscal policy — increasing the deficit in the short run — more urgent than ever. If we want to get back to pre-crisis unemployment rates (below 4.6%) anytime soon, the private sector isn’t going to be able to do it on its own, and certainly not with payroll tax increases and indiscriminate budget cuts weighing down already-insufficient growth rates:

While we are seeing some economic growth, the unemployment rate is not responding as strongly to the gains as it did in the past.

This slow job growth — today’s “jobless recovery” — isn’t an outlier. It’s a phenomenon that has been increasing over the last three decades, with jobs coming back more and more slowly after a downturn, even when GDP is increasing. The weak employment response has been an almost straight-line trend for more than 30 years.

Our institute’s newest econometric models show that each 1% boost in the GDP today will create, roughly, only a third as much improvement to the unemployment rate as the same 1% rise did in the late 1970s.

ShareThis

ShareThis